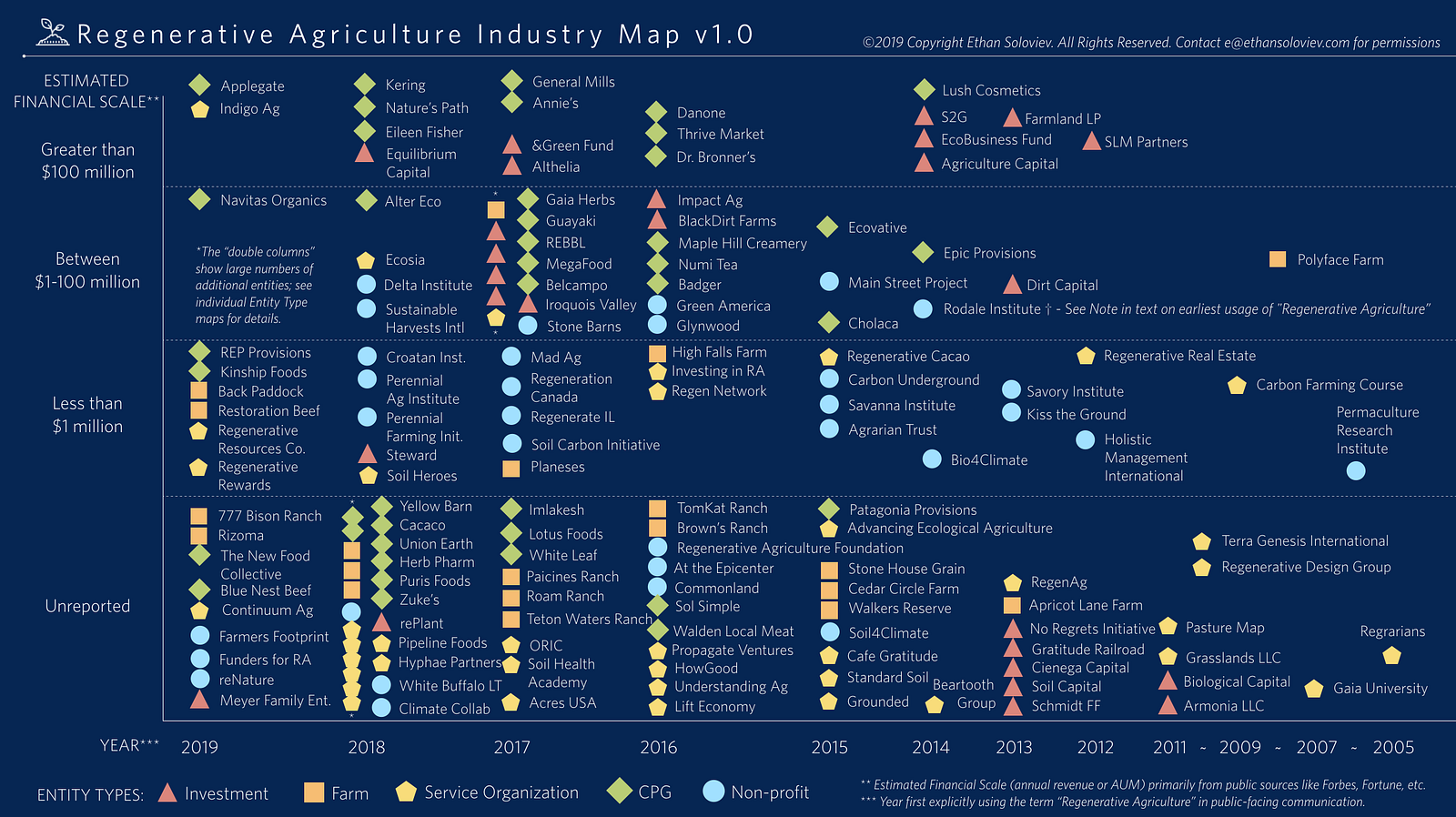

Welcome to the first graphical map of the Regenerative Agriculture Industry.

Companies, investors, organizations, and farms are included in this map based on the following criteria:

- They explicitly use the term “Regenerative Agriculture” or “Regenerative Farming” in public-facing communications.

- Or they invest financial capital into an entity meeting Criteria 1.

Hear Ethan & Koen discuss the map in the December ‘Investing in Regenerative Agriculture Podcast!

Why this criteria?

As I’ve described elsewhere, there are multiple divergent meanings of “Regenerative Agriculture” in use today. Instead of subjectively applying any particular definition, I’ve chosen to start with a simple objective approach: Who is using the term?

While this may seem overly simplistic, it turns out that even using the term is a non-trivial step for most organizations. It implies, at least, that the decision-makers have explored the definitional landscape and decided that something about “regeneration” is important enough to publicly align with and proclaim.

I recognize that this is a lowest-common-denominator approach, and invites onto this map entities whose usage of the term I disagree with — even entities whose approach I believe will degrade and banalize the deeper meaning of the term. Over time I will add more layers of analysis to discern between the different lineages and levels of regenerative agriculture that are sourcing each entity’s usage.

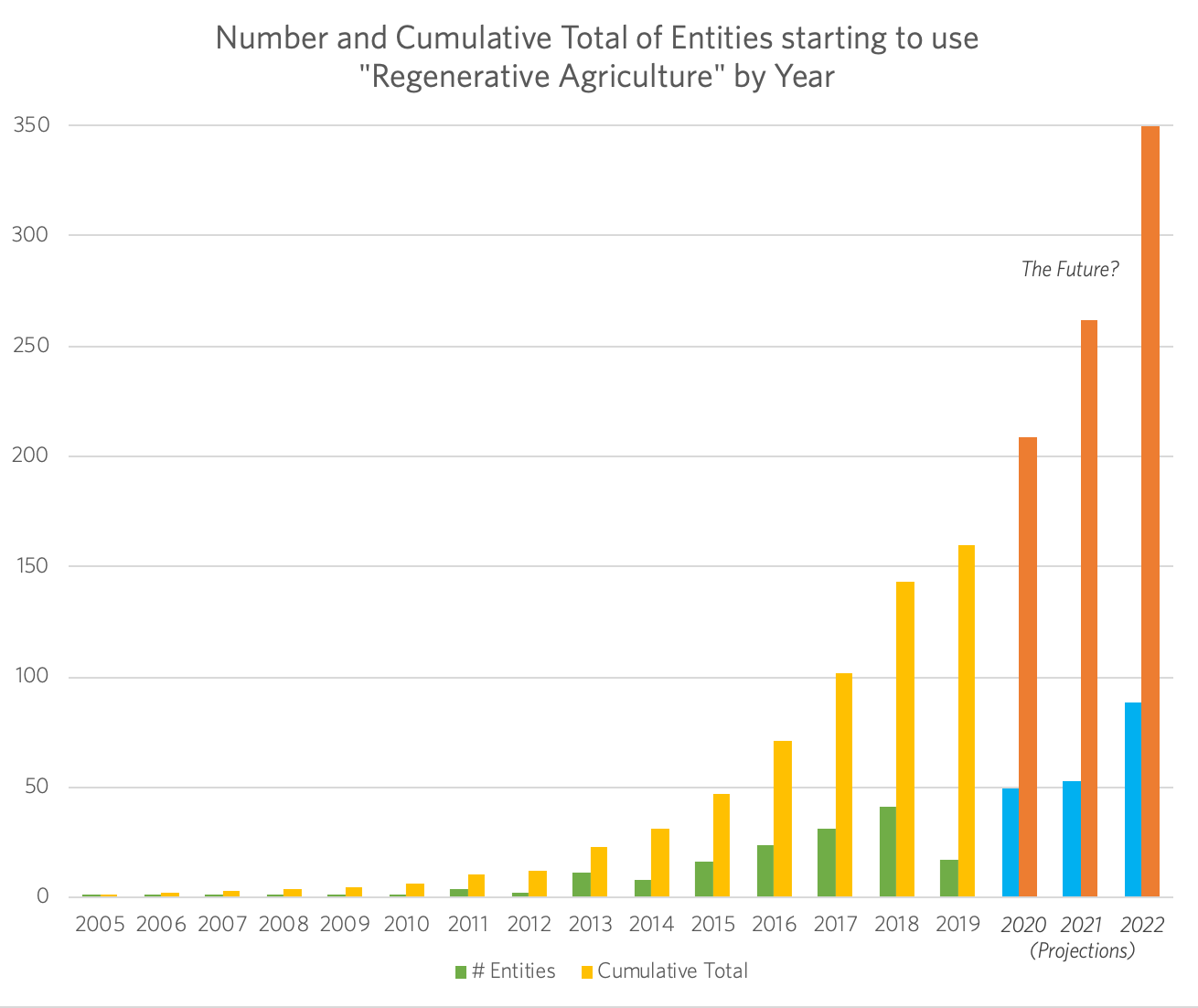

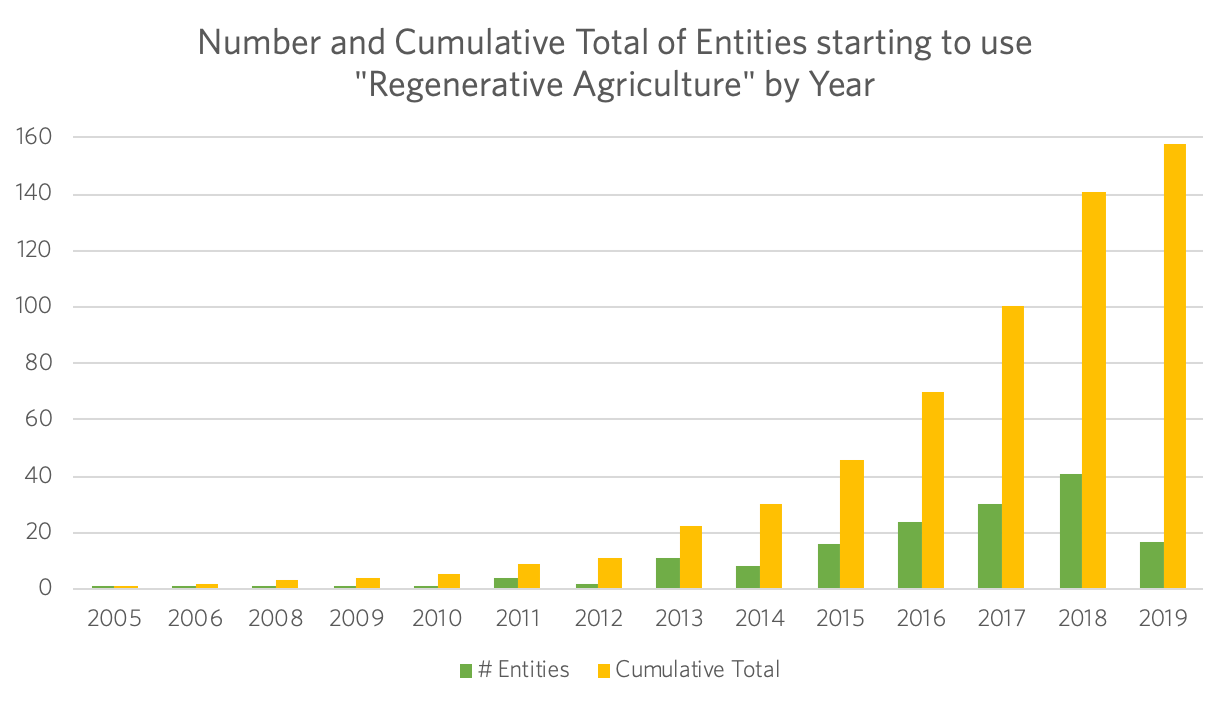

When I co-organized the Carbon Farming Course: Workshops in Regenerative Agriculture in 2009 and 2012, only a few small groups of organizations were using the term “Regenerative Agriculture”. Through a combination of pathways, these groups have exponentially grown the number of entities and financial scale of the industry. Through the uptake by large CPG companies starting in 2016, it’s likely that the annual revenue to companies that are explicitly promoting regenerative agriculture is greater than $50 billion.

This is a Draft

Version 1.0 is a draft. There are very likely mistakes. Please help me correct them. If the “usage year” listed for your organization is incorrect, I will happily change it — please just send me a link to the date of a public record where you use the term “Regenerative Agriculture”. If your estimated financial scale is incorrect, please tell me (with as much precision as you’d like to be public) what it should be. Thank you!

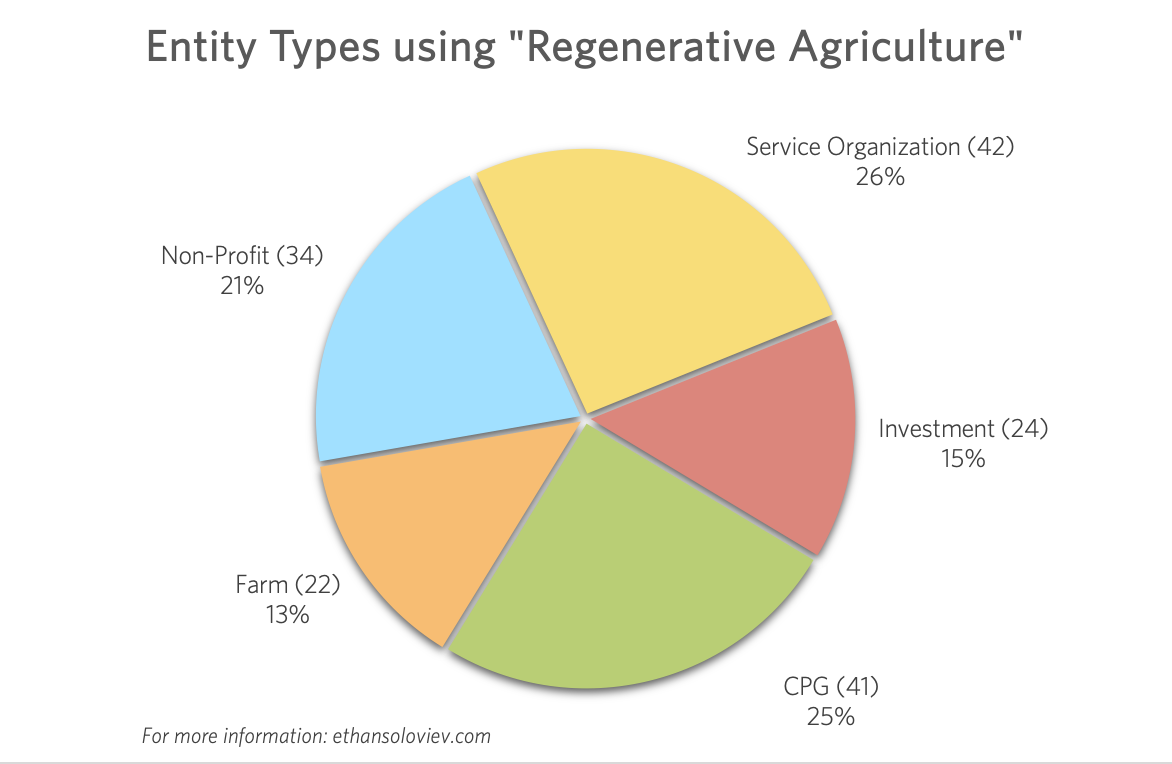

Entity Types

Organizations are grouped in five categories:

- Investment: Primarily investment managers and funds, though a few family offices are included.

- Farm: Includes farms that develop and market their own products. See additional note about Farms below.

- Service Organization: Educators, consultants, research organizations, agricultural equipment and product manufacturers, land managers not tied to a single farm, media producers, for-profit membership organizations, ecosystem platforms, and other types of organizations.

- CPG: Consumer Packaged Goods manufacturers, primarily food and beverage, but including some health and beauty products. Retailers of Consumer Packaged Goods are included here, along with fashion and clothing manufacturers.

- Non-Profit: A diversity of not-for-profit organizations, from education to research to events convening to advocacy.

There is significant overlap in the functional work of entities in the “Service Organization” and “Non-Profit” categories, with the primary division being the choice of legal organizational structure.

Strongly under-represented in Version 1.0 of the Map are farms. The number of farms that are beginning to use the term ‘regenerative’ is multiplying exponentially. Many farms that have been using the principles of Holistic Management, Biodynamics, Permaculture, or Organic Agriculture are now saying, “we have been regenerative for a long time.” Combine that with a flood of larger US and Australian farms that are growing conventionally while adopting some form of regenerative agriculture principles, and this is a challenging category to keep up with. This is compounded by the fact that a much smaller proportion of farms maintain up-to-date websites — which makes pinpointing the year they started using the term difficult.

In summary, the distinction that I’ve chosen for version 1.0 of the Map, “Explicitly using the term “regenerative agriculture” in public-facing communications” is hard to track for farms. And, I would like to do a better job in the next version of this map recording this quickly-changing farm. I’ll keep adding farms to the list, and welcome any contributions from the wider community.

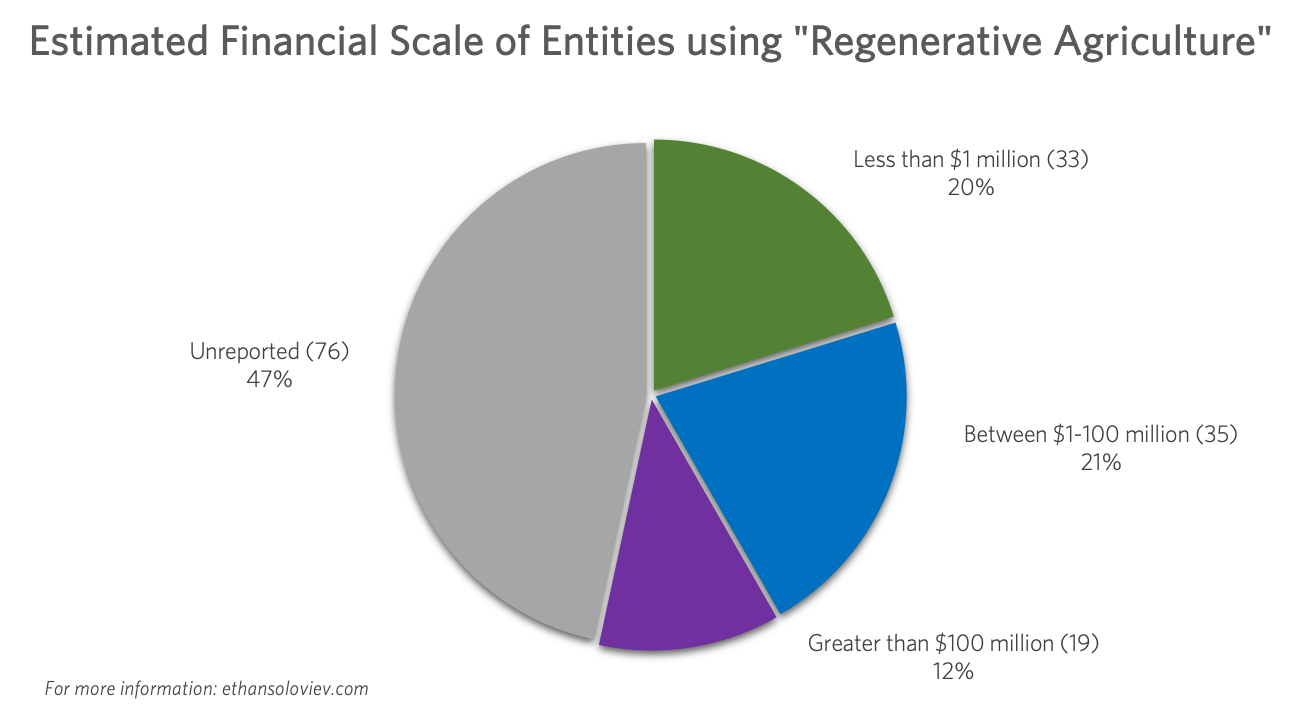

Estimated Financial Scale

Organizations are loosely clumped into one of 4 financial scale categories, based primarily on publicly available information. For most entities on the map the estimated financial scale refers to annual revenue, with the exception of Investment organizations where it refers to Assets Under Management (AUM).

One current issue with the map is that the estimated financial scale grouping is based on relatively current information (from the last 1–5 years), and does necessarily accurately depict the financial scale of the organizations at the time when they started using the term “Regenerative Agriculture.” I welcome any suggestions on a graphically elegant way to depict this complexity.

Note about Earliest Usages

This first written record of the term “Regenerative Agriculture” was in 1979 by Medard Gabel (thanks to Luke Smith of Terra Genesis for research on this). Soon afterwards (in 1983), Robert Rodale of the Rodale Institute began using the term, and led the creation of the “Regenerative Agriculture Association” sometime in the 1980s. They published at least one book that I have seen (“Booker T. Whatley’s Handbook on How to Make $100,000 Farming 25 Acres”), and began promoting early ideas about regeneration alongside their work on organic farming.

Sometime After Robert Rodale’s unexpected death in 1990, the Rodale Institute dropped the term, focusing on promoting Organic Agriculture for more than 20 years. After the permaculture community and several other organizations (especially Darren Doherty of Regrarians, Terra Genesis International, Armonia LLC, and Biological Capital) started using “Regenerative Agriculture” between 2009–2013, the Rodale Institute reclaimed the term (2014) in a modified usage that they continue today: “Regenerative Organic”.

Future Versions

There are two primary pathways along which I plan to develop I plan develop this map.

- Expansion. As noted, there are a lot of farms out there using the term that are not yet on this map. Additionally, this map is heavily United States-centric, and should definitely be expanded to better represent the work happening in South America, Europe, Africa, Asia, and Australia.

- Depth. I will add layers of detail and complexity over time. I’ll start with characterizing the “Lineages” from which each entity is sourcing their use of “Regenerative Agriculture”. Next I will characterize the Level of Regenerative Agriculture that each entity is working from, through a combination of supported self-reporting and my subjective assessments. Then I will start to develop more detailed attributes for the different entities, including the agricultural practices, business models, and metrics utilized by each. Eventually these attributes will include locations, climate zones, and crops produced.

If you would like to contribute to the development of either pathway, please email me to discuss: e@ethansoloviev.com.

Final Questions

Will the exponential growth trend of the last decade continue? How many entities using the term “Regenerative Agriculture” will it take to reverse climate change? What would success look like for the growth of this industry?

Will your company be the next added to the map?